Pennington County Assessor's Office

The County Assessor's Office is responsible for estimating the market value and determining the legislative classification of all property in Pennington County for real estate tax purposes. Valuations must meet the standards established by Minnesota Statutes and the Minnesota Department of Revenue.

Business Hours

Monday through Friday from 8:00 a.m. to 4:30 p.m.

218-683-7029

Notice:

MN Department of Revenue State Board of Equalization

Required Increases, under MN Statutes 273.061 subdivision 9(6)

City of Thief River Falls Commercial Land and Structures 10% Increase

Township of Norden Residential Land and Structures 5% Increase

Township of Norden Seasonal Residential Recreational Non-Commerical Land and Structures 5% Increase

Information and Resources

Information

The estimated market value and classification are based on the condition and use of the property as of January 2nd of each year. Notices of values and classes are mailed to the property owners in the spring of the year. If they disagree with the value or classification or have a question on the notice they received they should contact this office. If they feel they need to appeal the value or class further, there is information on the Notice as to the process. After the appeal process, the values and classifications are set and used for property tax for the following year. For personal property mobile homes, values and classifications are assessed for property tax the same year.

Click here for the Property Tax Calendar

Property Records Search – Property Cards

Homestead Classification

For your convenience, please find a blank copy of the Homestead Application below. In order to receive Homestead classification a homeowner must fully complete a Homestead Application and return to the Pennington County Assessor's office. Owners are not required to file a new application each proceeding year. However, the Pennington County Assessor's Office may require a new application or other information to verify the homestead status. Owner's are advised to inform the Assessor's Office within 30 days when vacating the property. New homeowners have until December 31st of the following year to file for homestead, provided they occupy the property by December 31 of the following year. Please contact the Pennington County Assessor's Office with any questions, (218) 683-7029.

Properties which are occupied as a primary residence by the owner or a qualified relative of the owner may qualify for a homestead. Occupants should contact the County Assessor's Office and fill out a homestead application or a relative homestead application. Homestead is a property tax reduction intended to keep taxes lower on owner/qualified relative occupied homes.

Special Homestead Applications:

- Homestead Exclusion Veteran with Disability Application

- Homestead Exclusion Surviving Spouse of a Veteran Application

- Homestead Exclusion Primary Family Caregiver Veteran Disability Application

- People who are blind/disabled class 1b Application

Special Program Applications and Verification Forms

Special Agricultural Homestead

Special Agricultural Homestead extends homestead treatment to:

- A property owner who does not live on the farm but actively farms the land.

- A qualifying relative who actively farms the land. (child, grandchild, sibling, or parent)

- Property held under a trust or property owned by an authorized farm entity.

More detailed information about requirements is contained with the applications.

Filing Requirements & Applications

Owners must enroll their property in the program every year with each county in which a Special Agricultural Homestead classification is requested by Dec. 31 of the current assessment year. If the property is not being farmed by the owner, the individual actively farming will need to complete and sign the application as well. If you have agricultural property in more than one county, make sure to apply in each county.

For changes in Agricultural property

If ownership, occupancy or other status changes occur, please use one of the following applications:

Special Ag Homestead - Entity Owned

Special Ag Homestead - Individually Owned

Special Ag Homestead - Trust Owned

For re-application with no changes in agricultural property, please use one of the following re-applications:

Special Ag Homestead - Entity Owned Reapplication

Special Ag Homestead - Individually Owned Reapplication

Special Ag Homestead - Trust Owned Reapplication

Common Questions

Do I Qualify for the Special Agricultural Homestead?

The agricultural property in question must be at least 40 acres. The person who owns the farm must be a Minnesota resident, not claim another Minnesota agricultural homestead and neither can their spouse. They must live within four townships or cities of the property.

The person who is actively farming the land must be a Minnesota resident, live within four townships or cities of the property and own the land, or be the spouse of the owner, the child of the owner, the child of the owner's spouse, or a sibling. The relationship can be by marriage or blood.

The person who is actively farming must participate in the day-to-day labor, decision making, and management of the claimed homestead. They also must assume all or part of the financial risks of the farm. The person does not have to live on the farm.

What Do I Need to Apply?

A completed application, available on this page or from the county assessor’s office. Owners who have applied and qualified in the previous year will get a re-application mailed to them every year around August. You must also provide a copy of your 156 EZ from the Farm Service Agency as well as your farm number.

Lastly, you must provide a copy of your Schedule F form or equivalent partnership / corporation form that were filed with the federal income tax return of the person actively farming. An affidavit from your tax preparer or attorney verifying that you have filed the form can be substituted instead of the form.

In some instances (i.e. multiple owners), separate applications must be submitted.

Please contact the Pennington County Assessor’s office with any questions at (218) 683-7029

Electronic Application Submission

Please create an account using your email address. Then select the appropriate application and fully complete. You will get an email notification when the application is submitted and accepted. Address changes and email address updates can also be submitted electronically using the Smart-File link.

Property Tax Exemptions

Property Tax Exemptions

What is a Property Tax Exemption?

A Property Tax Exemption is the elimination of all or a portion of the property taxes for a property that is legally eligible for that type of tax reduction.

Under Minnesota law, all real property (except for tribal lands) is presumed taxable. Since taxation is the rule and exemption is the exception, it is up to the property owner to prove that their property qualifies for exemption under Minnesota Statute § 272.02. A property can only become tax-exempt after the owner's exemption application has been approved by the county assessor.

Which properties are eligible for a Property Tax Exemption?

To be eligible for exemption, a property needs to meet two criteria:

- It needs to be owned by a qualifying person or entity, and

- It needs to be used for a public, educational, religious, or charitable purpose.

Some of the most common tax-exempt property types are:

- Churches or places of worship.

- Institutions of public charity.

- All properties used exclusively for public purposes, including public hospitals, schools, burial grounds, etc.

- Certain kinds of personal property, including in most cases property that creates energy, enables commerce, or conserves nature.

- Qualifying wetlands or native prairie lands.

- There are many other exempt property types also, besides those listed above. See Minnesota Statute § 272.02 for the longer list of exemptions.

When should I apply?

First-time applications should be filed as soon as possible after a property is acquired by a potential exempt organization. Qualified exempt organizations will need to acquire a property and use it for exempt purposes prior to July 1 of the current year in order for the property to be exempt from the next year's payable taxes.

The application review process can take one week to three months, depending on the complexity of the application.

How do I apply?

Fill out an application and compile the required paperwork.

Types of Exempt Applications (choose the one that best fits your organization):

- Exempt CR-PTE General Application (PDF): Please use this application if your organization is not an Institution of Purely Public Charity. The Standard Application is typically used by, though not limited to, churches, government agencies, and educational facilities.

- You will also need the following documents:

- Articles of Incorporation and Bylaws Certification from the IRS granting IRS Code 501(c)(3) status.

- IRS Form 990 Return and other financial income and expense statements.

- Property deeds and sale documents.

- Copies of tenant leases (if applicable).

- Any other relevant documents and records.

- Purely Public Charity Application (PDF): Please use this application if your organization is an Institution of Purely Public Charity (to help determine if your organization is a IPPC, or a non-profit as they are more commonly known, please see Minnesota Statute § 272.02 subd. 7).

- Nursing Home Application (PDF): Please use this application if your property is a Nursing Home (please see Minnesota Statute § 272.02 subd. 90 to help determine if you qualify as a Nursing Home).

Third Year Re-filing Requirement: If you are filing to satisfy the every-third-year re-filing requirement for a property that is already exempt, and the status of supportive documents filed with your initial application has not changed, then the only documents you need to send are:

- Your application.

- The last three completed years of the IRS 990.

Property Tax Refund

Property Tax Refund Instructions

- Check to see if you qualify. You may be eligible for a refund based on your household income and the property taxes or rent paid on your primary residence in Minnesota. For more information and/or to print the form & instructions, please go to Household Income for the Property Tax Refund | Minnesota Department of Revenue (state.mn.us)

- File your Property Tax Refund online at Online Services (state.mn.us)

- File your Property Tax Refund using a Software Product. Some tax software can electronically file the Property Tax Refund. Check your software for details and if theres questions, please contact their customer support.

- File your Property Tax Refund by paper using the M1PR Homestead Credit Refund (for homeowners) and Renter's Property Tax Refund.

- Check the status of your refund online by using the MN Department of Revenue: Where's My Refund? System at https://www.revenue.state.mn.us/filing-property-tax-refund.

The due date to file for your Property Tax Refund is August 15th. You may file up to one year after the due date.

For Questions on the Minnesota Property Tax Refund call 651-296-3781 or toll free at 1-800-652-9094

Free Tax Help is Available

For information about free tax preparation sites, go to www.revenue.state.mn.us and type Tax Help in the search box or

call 651-297-3724 or toll free at 1-800-657-3989

Mobile Homes & Travel Trailers

Overview

By state law, an appraiser must value personal property, which could include decks, additions, and travel trailers. If a trailer has current license registration it is exempt from personal property tax. If however, it does not display a current license, it must be valued as personal property and you will receive a tax statement for this personal property. This tax is due and payable in the same year.

Classification

Homestead is available for personal property mobile homes. Call the Pennington County Assessor's office at (218) 683-7029 to receive an application or download one from the Homestead tab on this page. Homestead applications are to be completed and returned to the assessor's office by May 29.

If the application is not returned it will result in a non-homestead classification.

To transfer the title of the mobile home, the taxes are to be paid in full. Please contact the Pennington County Treasurer's Office, (218) 683-7022, for a tax amount or estimate.

Frequently Asked Questions

1.What is an Estimated Market Value?

The Estimated Market Value (EMV) is what the assessor estimates your property would likely sell for on the open market. Minnesota Statute 272.03 Subdivision 8 defines market value as ‘the usual selling price at the place where the property to which the term is applied shall be at the time of assessment; being the price which could be obtained at a private sale or an auction sale, if it is determined by the assessor that the price from the auction sale represents an arm’s-length transaction. The price obtained at a forced sale shall not be considered.

2. How Does the Assessor Measure Market Value?

By reviewing the selling prices of similar properties in local areas. A Certificate of Real Estate Value is completed on all real estate transactions and a copy filed with the Assessor. By studying the certificates, Assessors have a good idea of what other properties will sell for. Another method of determining value is based on the current cost of replacement less all depreciation that has occurred.

3. Why Does My Value Increase When Nothing Has Been Done to My Property?

Supply and demand create market value and Assessors measure it. As demand increases and the cost of buying a particular property increases, other property values rise also. Your property becomes worth more, even though no improvements were made and you have no intention of selling it.

4. How Close to the “Actual” Value of a Property is the Assessors Value?

According to State Statutes, properties are to be assessed at Market Value. Because it is impossible to achieve 100% of market value on every property, the acceptable median sale range by state standards is from 90% to 105% of market.

5. What If I Think My Property is Over Assessed?

Assessment records are public information, and you can compare your assessment with other properties. If you have any questions, please call the Assessor’s Office. If you still disagree with the assessment, there are formal appeals you may take.

6. How can my value change every year?

The market values can and often do change every year. Reassessments and physical inspections are conducted at least once every five years. The State of Minnesota requires that county assessors conduct a sales ratio study every year in every area of the county. These studies show if the market values are too high or too low. Assessors are then required to adjust values to comply with the findings of the study. If the county does not respond appropriately the study’s results, the county may be required by the State to increase or decrease values after the appeal meetings. State increases or decreases may not be appealed by the property owner.

7. Why did my taxes go up even when my value went down?

This has been a very common scenario in recent years when the tax levies have increased but the valuations of properties have decreased. Keep in mind that values are only one part of the tax equation. Here’s a simple example: If all property values in a city go down 10% but the amount that the city needs in taxes goes up 3%, then each property’s tax bill would likely go up by 3% if all other factors are held constant. This is because the share of the tax burden on each parcel has remained the same when taxes increased.

8. What are the approaches to valuing property?

Assessors may use three approaches or methods to value property. These are the cost approach, the sales comparison approach, and the income approach. The cost approach considers the cost to build and develop a property and then removes depreciation due to age and other factors. This method is usually more reliable on newer improvements.

The sales comparison approach utilizes sale prices of similar properties as a measurement of market value. This is often used in property tax assessment since it is an easily explainable and reliable way to show value, especially for residential and seasonal property.

The income approach converts the anticipated benefits of future income and sale of a property into a present value. This is most commonly used for commercial, industrial, and apartment property since income is a primary reason for ownership of these properties.

9. Why do some parcels with similar values have huge differences in tax amounts?

This question has a complex answer that cannot be fully explained here. The primary and most common reason for big differences would be due to classification. For example, an agricultural homestead has a much lower tax rate than most others. The ag homestead classification also has additional tax credits that other classifications do not receive.

Another reason for large differences is due to the local tax rate. This rate is determined by the County Auditor. The rate is less in areas with more market value and lower tax levies.

10. If I purchase a property for less than the Estimated Market Value, will my value go down?

The Estimated Market Value (EMV) doesn’t automatically go down because someone pays less than the County’s EMV. The EMV is set based on a group of sales and not a single sale, even if the sale is open market. When many properties in one area sell for more than the assessor’s value, then the assessor raises values. In property tax assessment, care is taken to treat similar properties equally so that owners are not paying an incorrect tax amount.

Appeals Process

Steps to Appeal

If you have a dispute with your assessed value(s):

- Collect facts to show why your market value seems wrong, (for example: recent appraisal or view recent county sales of like properties from our Recent Sales tab).

- View the Frequently Asked Questions tab.

- If you still have questions, contact the Assessor's Office at: (218) 683-7029.

- Visit the Assessor's Office at: 101 Main Ave N, Thief River Falls, MN 56701.

If still not resolved:

- Attend the Open Book meeting or Local Board of Appeal & Equalization meeting listed on your value notice.

- From the Open Book meeting and the Local Board meeting, you can appeal further at the County Board of Appeal & Equalization.

Finally, if you still have a concern:

- You may petition with Minnesota Tax Court.

- Tax petitions may be filed after you receive your value and before April 30th of the year the taxes are payable.

For more information please visit the MN Department of Revenue Appealing Property Value and Classification page.

Disaster Relief

Homestead and non-homestead property(s) may be eligible for tax relief if a structure has sustained damage of at least 50 percent in value due to fire or natural disaster.

The program allows for a maximum of 12 months of property tax credit, which is for the full calendar months the property is not usable.

Property owners should notify the Pennington County Assessor's Office when the disaster occurs and then apply for the credit at the time they begin reuse of the property.

More information about the program may be found on the Department of Revenue's fact sheet.

Senior Citizen Property Tax Deferral

This program allows people 65 or older, whose household incomes are $60,000 or less, to defer a portion of their homestead property taxes.

The deferred taxes accrue as a lien on the property and are due within 90 days after the property is sold, transferred, or no longer qualifies as a homestead.

Applications are available online or from the Pennington County Assessor's office, and are due to the Minnesota Department of Revenue by July 1 to defer a portion of the taxes you owe for the next year.

More information about the program may be found on the Department of Revenue's fact sheet, provided below.

Senior Citizen Deferral Fact Sheet

https://www.revenue.state.mn.us/property-tax-deferral-senior-citizens

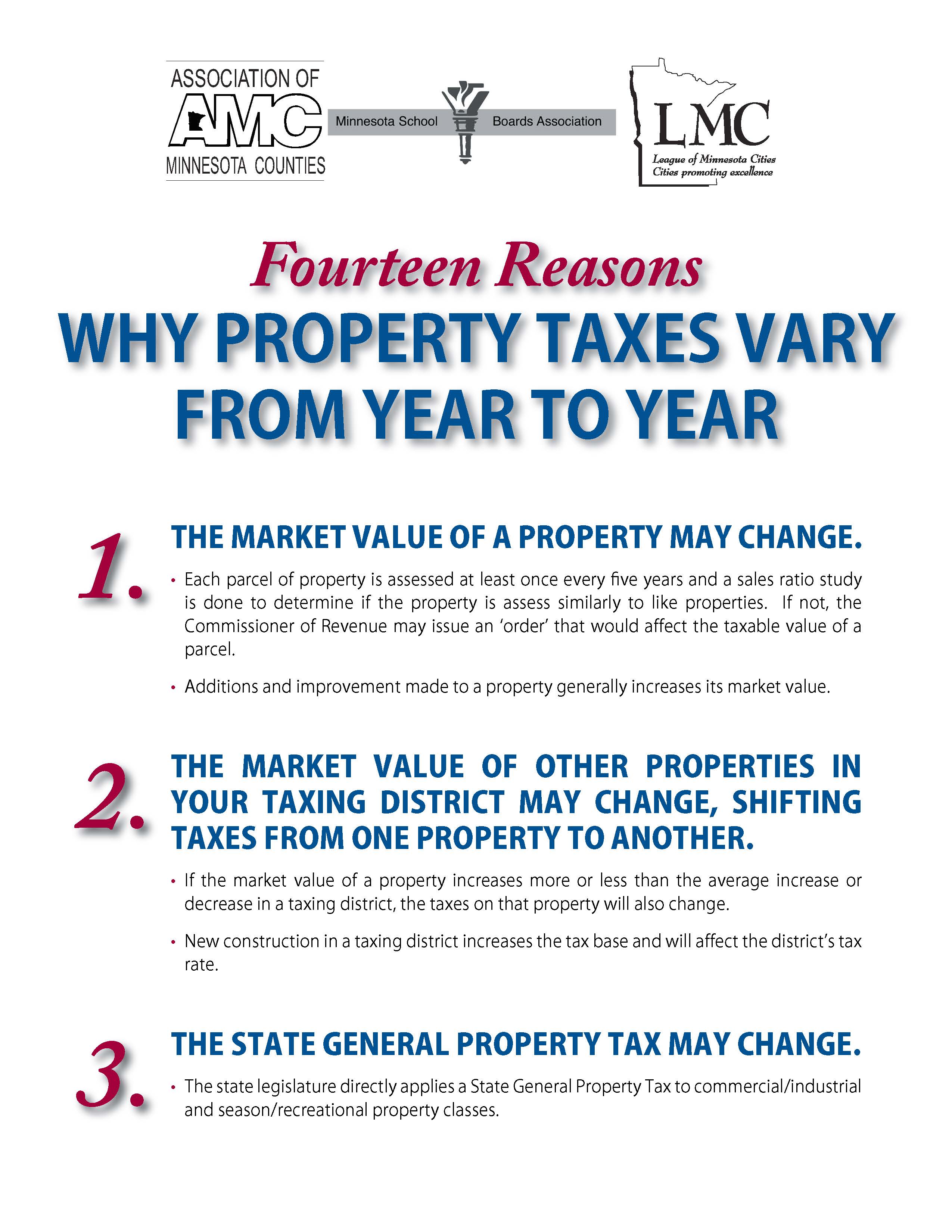

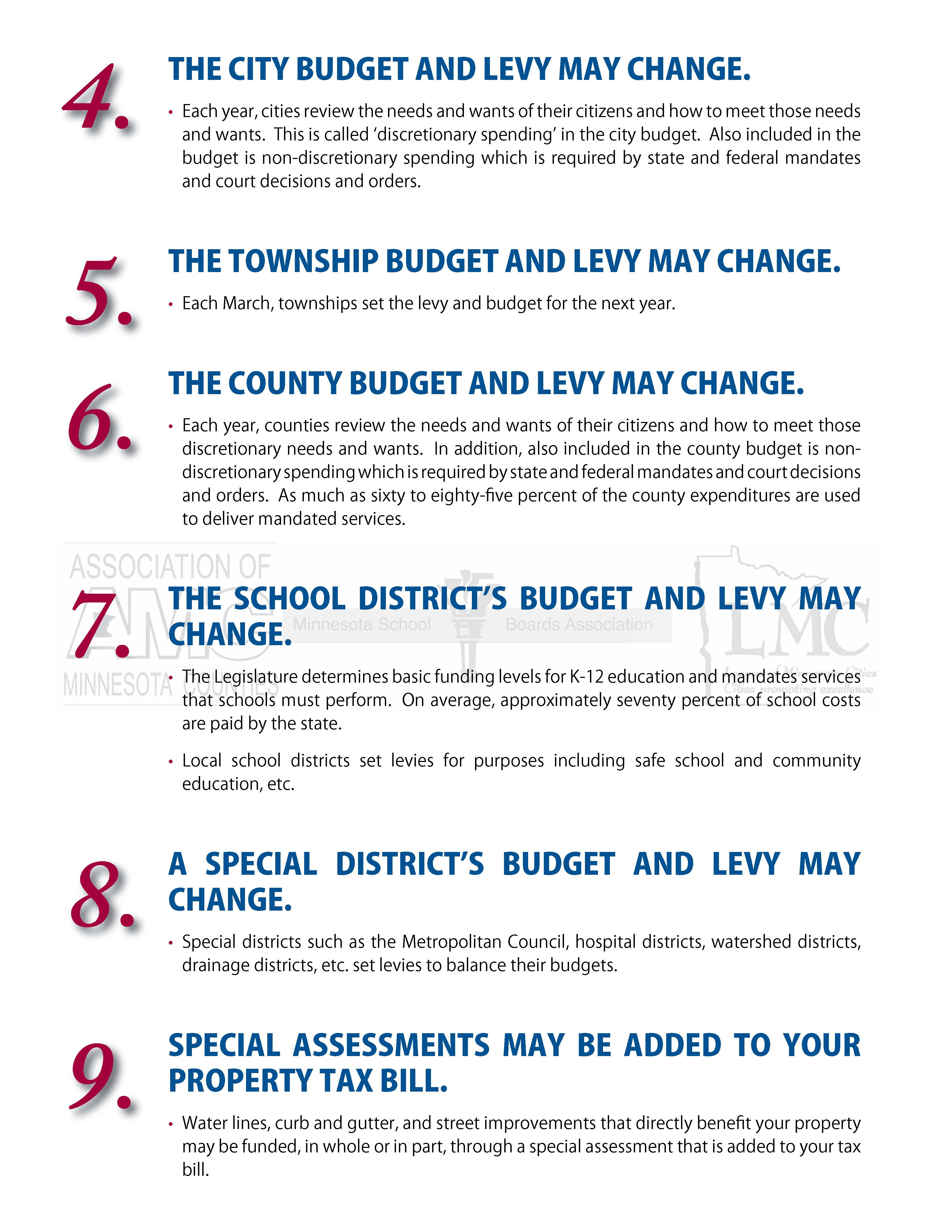

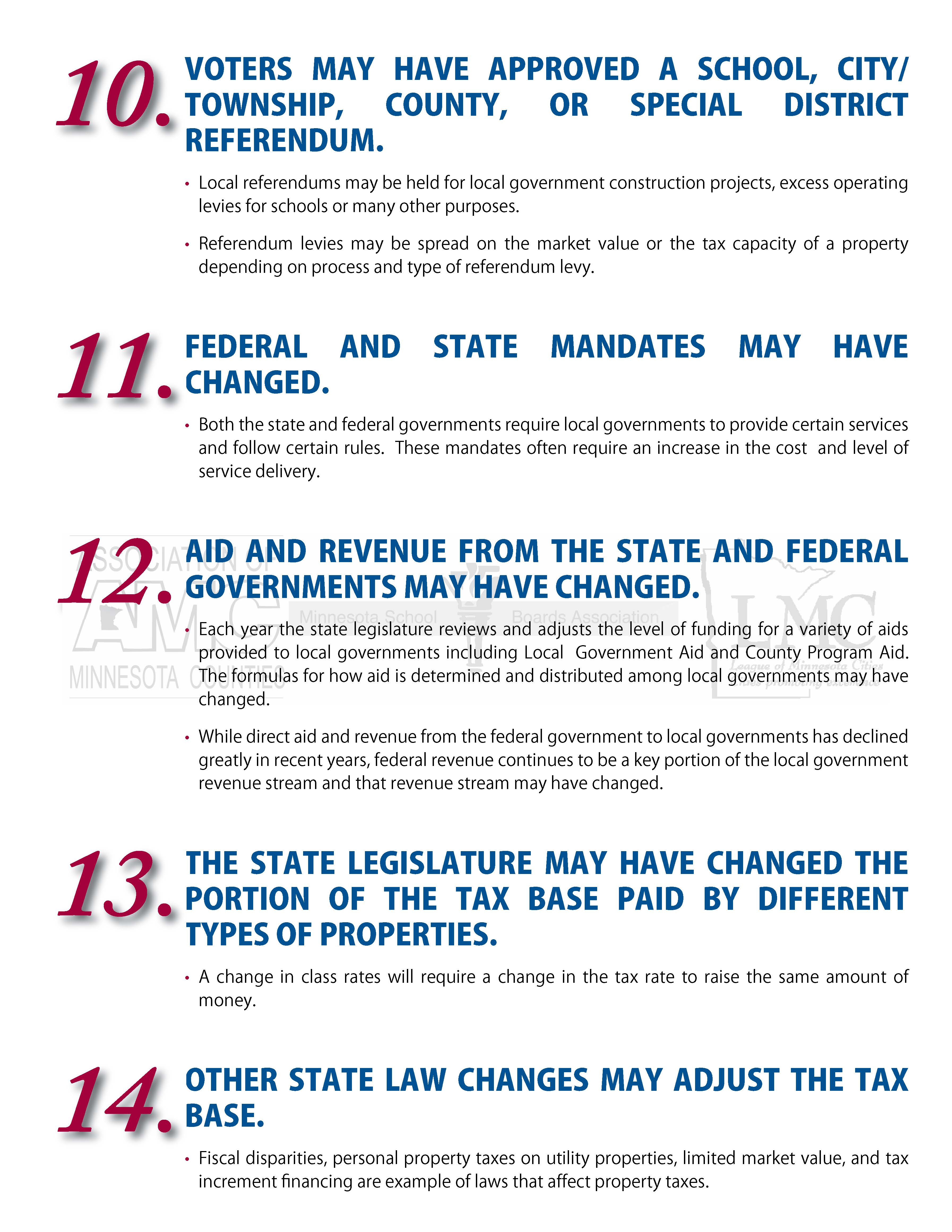

14 Reasons Why Property Taxes Vary From Year to Year

Carl Bruzek

County Assessor

Pennington Government Center

PO Box 616

101 Main Ave N

Thief River Falls, MN 56701

Phone: 218-683-7029

Fax: 218-683-7026

Email

Ashley Benson

Senior Assessor/Appraiser

Pennington Government Center

PO Box 616

101 Main Ave N

Thief River Falls, MN 56701

Phone: 218-683-7029

Fax: 218-683-7026

Email

Amber Vareberg

Deputy Assessor/Appraiser

Pennington Government Center

PO Box 616

101 Main Ave N

Thief River Falls, MN 56701

Phone: 218-683-7029

Fax: 218-683-7026